Regression to the mean cub. Understanding regression to the mean. Application in the world of finance

Do you believe that after great luck there is always a streak of bad luck? For example, if today you received a really strong deal in poker, then tomorrow even the machine that dispenses shoe covers will ignore you. Or maybe you think that your talent for cutting with a jigsaw or your unearthly beauty must be inherited by your children? If you are sure of this, then statistics speak out more restrainedly on this issue. A statistical principle called “regression to the mean” will help explain such phenomena. Ignoring it can lead to, at a minimum, a bad mood, and at a maximum, to complete disappointment in one’s life. Actually the idea is very simple. Let's sort it out.

Talent or genius, great luck, failure or other extraordinary phenomenon are extremely rare, that is, the likelihood of their occurrence is extremely small. The probability of a repetition of such a rare event will be even less, since probability multiplication is used to find it. Thus, after any extreme event (good or bad), everything returns to normal. There is a very important point here - life does NOT compensate for your failures or victories, it’s just that your luck indicators rush towards their average values. This is regression to the mean (from the Latin regressio - reverse movement). The same thing happens with the change of generations. Your children will definitely be talented, but most likely in a different area.

The concept of regression was first introduced by Sir Francis Galton, an English generalist researcher. He is responsible for another fundamental concept of statistics – correlation. While studying heredity, Galton measured everything that could be measured in his compatriots: heads, noses, hands, the number of fussy movements, the degree of attractiveness, etc. Galton believed that a person’s character, his mental abilities and talent are also determined by heredity and are subject to the principle of normal distribution.

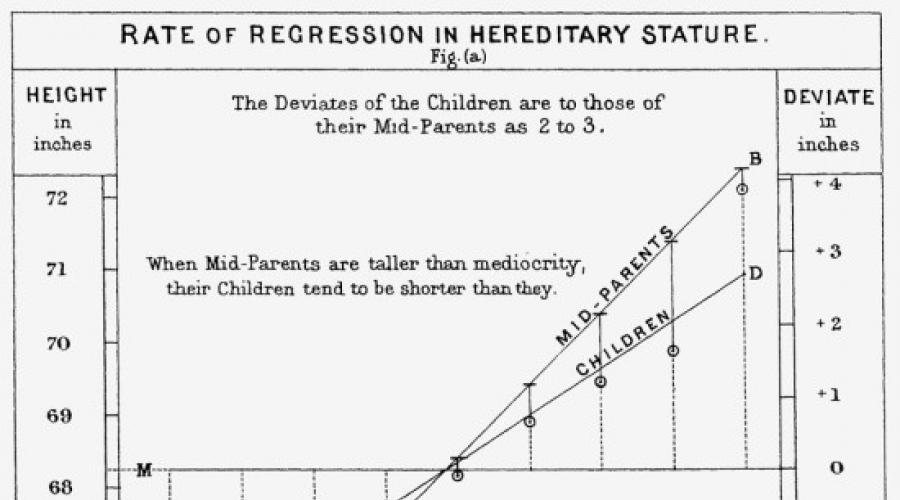

In one of his works, he tried to find a connection between the height of parents and the growth of their children. The dependence is obvious - tall parents give birth to tall children and vice versa. But Galton, in addition to this, also discovered some not entirely logical patterns. For example, he found that parents with above average height had tall children, but they were not as tall as their parents. And parents with below average height had children who were short, but not shorter than their parents. This means that the height of adult children deviates less from the average than the height of their parents. That is, descendants “regress” more strongly to the mean. Actually, Galton called this phenomenon “regression to mediocrity,” which more accurately reflects the meaning, IMHO.

Galton constructed a graph that resembles a modern scatterplot.

He divided people into groups depending on their height (in inches), calculated the arithmetic mean for each group and marked these values on the graph. Next, Galton approximated these points and constructed straight lines, the so-called regression lines. Galton even calculated the correlation coefficient - 2/3. This means that only 67% of children's height is determined by the height of their parents.

The graph reads: “When the average height of parents is greater than the average height of the population, children tend to be shorter than their parents. Conversely, when the average height of parents is less than the population average, children tend to be taller than their parents.”

Although Galton's conclusions and ideas are now mildly questioned rather than criticized, they have revolutionary significance for statistics. Thanks to this versatile scientist, regression and correlation analyzes are now widely used.

Below we have constructed a scatterplot (aka scatterplot) for the data collected by Galton. In 1886, he presented a tablet showing the heights of 928 adult children and the heights of their 205 parents (a weighted average of the heights of the father and mother). Since then, this data has often been used as an excellent example of regression to the mean.

Understanding Regression to the Mean

Whether overlooked or misexplained, the phenomenon of regression is foreign to the human mind. Regression was first recognized and understood two hundred years later than the theory of gravity and differential calculus. Moreover, it took one of the finest British minds of the 19th century to explain the regression.

This phenomenon was first described by Sir Francis Galton, Charles Darwin's second cousin, who had truly encyclopedic knowledge. In a paper entitled "Regression to the Mean in Inheritance," published in 1886, he reported measuring several successive generations of seeds and comparing the heights of children with the heights of their parents. He writes about seeds like this:

“The research yielded an interesting result, and on the basis of it, on February 9, 1877, I gave a lecture to the Royal Association. The experiments showed that the offspring did not resemble the parents in size, but always turned out to be more ordinary, that is, fewer large parents or more small ones... The experiments also showed that, on average, the regression of the offspring is directly proportional to the deviation of the parents from the mean.”

Galton apparently expected the learned audience at the Royal Association, the world's oldest independent research organization, to be as surprised by his "interesting results" as he was. But the most interesting thing is that he was surprised by the usual statistical pattern. Regression is ubiquitous, but we do not recognize it. She's hiding in plain sight. Within a few years, with the help of the eminent statisticians of his time, Galton went from the discovery of hereditary regression of size to the broader understanding that regression inevitably occurs when there is incomplete correlation between two quantities.

Among the obstacles the researcher had to overcome was the problem of measuring regression between quantities expressed in different units: for example, weight and ability to play the piano. They are measured by taking the entire population as a standard for comparison. Imagine that 100 children from all grades of primary school were measured for their weight and play ability and ranked the results in order, from the maximum to the minimum value of each indicator. If Jane is third in music and twenty-seventh in weight, you can say that she is better at playing the piano than she is tall. Let's make a few assumptions for simplicity.

Any age:

Success in playing the piano depends only on the number of hours of practice per week.

Weight depends solely on the amount of ice cream consumed.

Eating ice cream and the number of hours of music lessons per week are independent variables.

Now we can write some equations using list positions (or standard scores as statisticians call them):

weight = age + ice cream consumption playing piano = age + hours of practice per week

Obviously, when trying to predict piano performance by weight, or vice versa, regression to the mean will appear. If all we know about Tom is that he is a twelfth in weight (much above average), we can statistically conclude that Tom is probably older than average and probably consumes more ice cream than others. If all we know about Barbara is that she is eighty-fifth in piano (well below the group average), we can conclude that Barbara is most likely still young and probably practices less than others.

The correlation coefficient between two quantities, ranging from 0 to 1, is a measure of the relative weight of the factors influencing both of them. For example, we all share half of our genes with each of our parents, and for traits that have little external influence (such as height), the correlation between parent and child is close to 0.5. To evaluate the value of the correlation measure, I will give several examples of coefficients:

The correlation between the sizes of objects accurately measured in metric or imperial units is 1. All determining factors affect both measurements.

The correlation between self-reported weight and height for adult American men is 0.41. If women and children are included in the group, the correlation will be much higher because an individual's gender and age influence their assessment of their height and weight, which increases the relative values of the common factors.

The correlation between high school academic ability tests and college GPA is approximately 0.60. However, the correlation between aptitude tests and graduate success is much lower - largely because the level of ability in this group does not vary much. If everyone's abilities are approximately the same, then the difference in this parameter is unlikely to greatly affect the measure of success.

The correlation between income and educational attainment in the United States is approximately 0.40.

The correlation between a family's income and the last four digits of their phone number is 0.

It took Francis Galton several years to understand that correlation and regression are not two different concepts, but two perspectives on one. The general rule is quite simple, but it has surprising consequences: in cases where the correlation is not perfect, regression to the mean occurs. To illustrate Galton's discovery, let's take a suggestion that many find quite curious:

Smart women often marry less intelligent men.

If at a party you ask your friends to find an explanation for this fact, then you are guaranteed an interesting conversation. Even people familiar with statistics will interpret this statement in causal terms. Some will think that smart women seek to avoid competition from smart men; someone will assume that they are forced to make compromises when choosing a spouse due to the fact that smart men do not want to compete with smart women; others will offer more far-fetched explanations. Now think about the following statement:

The correlation between spouses' intelligence scores is not perfect.

Of course, this statement is true - and completely uninteresting. In this case, no one expects perfect correlation. There is nothing to explain here. However, from an algebraic point of view, these two statements are equivalent. If the correlation between spouses' intelligence scores is not perfect (and if women and men do not differ on average in intelligence), then it is mathematically inevitable that intelligent women will marry men who are, on average, less intelligent (and vice versa). Observed regression to the mean cannot be more interesting or more explainable than non-ideal correlation.

One can sympathize with Galton - attempts to understand and explain the phenomenon of regression are not easy. As statistician David Friedman ironically notes, if the issue of regression arises in a trial, the party that has to explain it to the jury is sure to lose. Why is this so difficult? The main reason for the difficulty is mentioned regularly in this book: our minds are prone to causal explanations and do not cope well with “simple statistics.” If some event attracts our attention, associative memory begins to look for its cause, or rather, any reason already stored in memory is activated. When regression is discovered, causal explanations are sought, but they will be incorrect, because in fact regression to the mean has an explanation, but there are no reasons. One of the things that comes to our attention during golf tournaments is that athletes who play well on the first day often play worse afterwards. The best explanation is that these golfers got unusually lucky on the first day, but that explanation lacks the force of causality that our minds prefer. We pay good money to those who come up with interesting explanations for regression effects for us. A commentator on a business news channel who correctly remarks that “this year was better for business because last year was bad” will likely not last long on the air.

Our difficulties in understanding regression arise from both System 1 and System 2. Without further instruction (and in many cases, even after some familiarity with statistics), the relationship between correlation and regression remains unclear. It is difficult for System 2 to understand and internalize it. This is partly due to System 1's insistence on providing causal explanations.

Three months of using energy drinks to treat depression in children produces significant improvements.

I made up this headline, but what it describes is true: Giving energy drinks to depressed children over a period of time shows clinically significant improvement. Similarly, children with depression who stand on their heads for five minutes or pet cats for twenty minutes every day will also show improvement. Most readers of such headlines will automatically conclude that the improvement was due to the energy drink or petting the cat, but this is a completely unfounded conclusion. Depressed children are an extreme group, and such groups regress toward the mean over time. The correlation between depression levels across successive tests is imperfect, so regression to the mean is inevitable: Children with depression will get a little better over time, even if they don't pet cats or drink Red Bull. To conclude that an energy drink - or any other treatment - is effective, it is necessary to compare a group of patients receiving it with a control group receiving no treatment at all (or, better yet, a placebo). The control group is expected to show improvement due to regression alone, and the purpose of the experiment is to find out whether patients receiving treatment improve more than is explained by regression.

Incorrect causal attributions of the regression effect are not limited to readers of the popular press. Statistician Howard Weiner compiled a long list of prominent researchers who made the same mistake, that is, confusing correlation with causation. The regression effect is a common source of problems in research, and experienced scientists develop a healthy fear of pitfalls, that is, unwarranted causal inferences.

One of my favorite examples of error in intuitive predictions comes from Max Bazerman's excellent book, Value Judgments in Management Decision Making, and is adapted from:

You are forecasting sales in a chain of stores. All stores in the chain are similar in size and assortment, but their sales volume varies due to location, competition and various random factors. You were presented with the results for 2011 and asked to determine sales in 2012. You are instructed to stick to economists' general forecast that overall sales growth will be 10%. How would you complete the following table?

After reading this chapter, you know that the obvious solution to add 10% to each store's sales is wrong. The forecast should be regressive, that is, for stores with poor results you should add more than 10%, and for the rest - less, or even subtract something. However, most people are puzzled by this task: why ask about the obvious? As Galton discovered, the concept of regression is not obvious.

From the book Psychoanalytic Diagnostics [Understanding personality structure in the clinical process] author McWilliams NancyExpressive technique: supporting individuation and preventing regression People with a borderline level of personality organization need empathy no less than others, but their changes in mood and fluctuations in ego state make it difficult for the doctor to understand when and where it should be given

From the book Introduction to Psychoanalysis by Freud SigmundTWENTY-SECOND LECTURE. Concept of development and regression. Etiology Dear ladies and gentlemen! We have learned that the libido function undergoes a long development before it begins to serve procreation in a way called normal. Now I'd like to show you

From the book Social Influence author Zimbardo Philip GeorgeUnderstanding Paying attention to a message whose meaning is not entirely clear is like eating a portion of cotton candy that has neither full-fledged materiality nor any lasting meaning. At a minimum, we must understand and take note of the general

From the book Basics of Hypnotherapy author Moiseenko Yuri IvanovichAge Regression Method This method involves taking the patient in a trance state into the past so that he can recall a repressed traumatic memory or affect. The phenomenon of age regression is such that, turning the hands of the clock back, being transported to

From the book Orders of Help by Hellinger BertUnderstanding Participant: We are talking about a patient who is about 40. She is married and has two children (a nineteen-year-old son and a fourteen-year-old daughter). This family is from Lebanon. She has severe migraines and suffers from depression. The marriage is very bad. The wife found out that her husband twenty years ago

From the book Personality Theories and Personal Growth author Frager RobertUnderstanding Rogers identifies three types of understanding that are found in psychologically mature people when perceiving reality. These are subjective understanding, objective understanding and interpersonal understanding. Subjective understanding is the most important, it includes

From the book SCHIZOID PHENOMENA, OBJECT RELATIONSHIPS AND SELF by Guntrip HarryThe fight against regression (1) A decisive movement in the opposite direction. We have argued that, left to his own devices, the individual can only “help” his regressed ego with his illness, or, alternatively, he can try to suppress the regressed ego.

From the book On You with Autism author Greenspan StanleyChapter 27 Breakdowns and Regressions A breakdown is, in essence, a complete loss of control over your emotions. How can we help a child who falls to the floor, screams, hits his head, tries to hit his mother or father, or runs around uncontrollably and screams, especially if he is a child with

From the book Think Slow... Decide Fast author Kahneman DanielRegression to the Mean One of the most powerful insights of my career occurred while teaching Israeli Air Force instructors the psychology of effective teaching. I explained to them an important principle of skill training: Rewarding for improvement works.

From the book Intelligence: instructions for use author Sheremetyev KonstantinTalk about regression to the mean “She says she knows from experience that criticism is more effective than praise. But she doesn't understand that all of this is simply the result of regression to the mean." "Perhaps we were less impressed with the second interview because the candidate was afraid of us

From the book A completely different conversation! How to turn any discussion into a constructive direction by Benjamin BenUnderstanding another I don't get upset if people don't understand me, I get upset if I don't understand people. Confucius When meeting another person, think about how mysterious a thing can happen now. You can know the other person's thoughts, feel his feelings, enjoy

From the book Kafka's Dismemberment [Articles on Applied Psychoanalysis] author Blagoveshchensky Nikita AlexandrovichUnderstanding The first type of awareness is simply understanding something specific that you would like to change. Often people are completely unaware of their unconstructive habits, including unhelpful communication methods, even when they are obvious to others. We discussed

From the book Ideal Negotiations by Glaser JudithMasyanya as a mirror of Russian regression[**] 1. Warnings Firstly, I would like to immediately state that I do not intend to offend anyone with the term regression. As you know, in psychology there are no offensive words at all. This is especially true for psychoanalysis, where grandiose-exhibitionist

From the book Family Systems Theory by Murray Bowen. Basic concepts, methods and clinical practice author Team of authorsStep 3: Understanding Subsequent sessions with Brenda focused on getting her to know what people really think—she needed to learn to see the world through their eyes, not just her own. When will we understand what it means to “be in another person’s place” and what it means?

From the book The Big Book of Psychoanalysis. Introduction to psychoanalysis. Lectures. Three essays on the theory of sexuality. Me and It (collection) by Freud SigmundManifestations of Regression The process of regression depends on such a complex conglomeration of forces that it is not yet possible to figure out which of them is the most important. During this process, the person is exposed to a certain type of anxiety. The person is emotionally reactive

From the author's bookTwenty-second lecture. Concept of development and regression. Etiology Dear ladies and gentlemen! We have learned that the libido function undergoes a long development before it begins to serve procreation in a way called normal. Now I'd like to show you

What can be identified as the main, statistically reliable unit of market characteristics? Regardless of the type of transaction (binary options, forex, stock markets, futures, etc.), regardless of the type of asset (currency, stocks, indices, commodities), we can talk about one rule - the market never moves in one direction. His movements are always oscillatory. It is on this property that “regression to the mean” is built.

What is regression to the mean

Regression back to the mean is a statistical value that indicates that the positive (negative) heights achieved are extreme. As a result, we can expect a rollback to the average values.

This pattern is not financial or market. It is applicable to any industry. Let's take sports for demonstration. If a team has a lot of successful games now, then most likely there will be fewer successful games in the future. that is, overvaluation and regression to the mean. The best non-financial demonstration of this occurred in 2016 in English football. The Leicester club, which throughout its history has never risen above 10th place in the championship, won the championship. But already in the next season he returns to his usual level. Again we see overvaluation and regression. Although from the point of view of what the “financial gurus” tell us, this was the birth of a new trend...

Application in the world of finance

Similar examples can be found in the financial world. For example, if an exchange (asset) is in excessively high demand, next year there will most likely be a decline in this activity. No matter how strong the trend is, sooner or later it will turn into an opposite movement or a strong correction. Here's an example from a live chart.

And this applies to any market and any element of it. If some option (futures, stock) has an extremely low value, then most likely it is simply undervalued and has a statistical probability of regressing towards growth. The situation is exactly the same with assets that everyone wants to trade and for which quotes have suddenly risen sharply - most likely they will experience regression, but this time in the direction of decreasing prices.

How regression can be used in Forex and binary options

In training, I often bring up the issue of market regression, because in my humble opinion, this is a fundamental thing that every trader should learn. But this is not what we are talking about now, but the fact that I noticed an amazing pattern - 90-95% of traders have a short vision. They look at the current situation, at least a few candles forward and back. But this is not trading. This is luck, fortune, coincidence... Anything, but not trade. Ultimately, why do the same 90-95% of traders lose? I'm not saying it's just a matter of market regression, but it's one of the factors. If you do not take it into account, you are trading at random and sooner or later you will merge.

PAMMs, signalers and hedgehogs with them

Now a few words about practice. All traders are looking for signals, signalists, analysts, PAMM accounts, and so on. What do they pay attention to? Profitability of signals/trading. The higher the better. Moreover, in Forex this phenomenon has been taken to the point of insanity - they give a rating for 1 week. But this is not a statistically significant value. Example. There is a trader who has had a profitability of +450% of his deposit over the last week. He tops the ratings and everyone wants to subscribe to him. And everyone is pouring money together. Why? Yes, because this same trader can trade for a year with an average weekly deposit profitability of $100. That is, his indicator +450 is an overestimated indicator, and then regression follows.

Remember what Buffett said? Always buy undervalued assets and buy overvalued ones. Such a simple secret to success.

Let me give you an example with our trading signals. At the beginning of each day, I draw up a trading plan, comparing the statistical results for the entire period (this is approximately 2 years) and the results for yesterday, and so on for each strategy. Here's what it looks like today using strategy #2.

I will consider 3 options:

- AUDUSD. For the entire period, the profitability on 1 candle is 53%. Yesterday 33%. The conclusion is that profitability is underestimated. I can safely trade using such signals.

- USDJPY. FOR the entire period, the profitability for 1 candle is 56%, and for yesterday - 75%. Conclusion - the signals for this asset worked abnormally well yesterday. We are waiting for regression to the average values, so we do not trade this asset (alternatively, we trade in the direction opposite to the signal).

- USDCAD. Profitability for the entire period for 1 candle is 51%, and for yesterday’s day 50%. Conclusion - the figures are comparable, the asset has not made any sharp leaps in terms of profitability. If you trade purely by regression, you cannot trade the balance on USDCAD.

These are 3 situations, there cannot be others. This is what these 3 assets look like for me at 17:00 on a business day.

If you break the limit or, conversely, sponsor every second player at the tables, know that sooner or later you will fall back to the “average”. we'll talk about how you can use simple metamathematics to easily explain your results.

Take any action in which there is (1) an element of luck and (2) an imperfect indicator of interest. For example, let's take the percentage of hits in baseball. Each player has some ability that is unique to him, but we cannot measure it in any way. Instead, we look at results, which are an imperfect and simplistic measure of these abilities, since they are random in nature: a lucky bounce or wind direction are all out of the player's control.

Regression to the mean tells us that those who hit the ball well in one season tend not to hit the same ball the next year. This is because the outstanding performance we look at is partly down to luck, which throws the balance off balance. An average player performs outstandingly in one season and, of course, overestimates his true abilities. Next year he won't be as outstanding because the likelihood of him continuing to get lucky is extremely low.

The same goes for “losers.” Poor performance usually underestimates a player's true ability, because in a given season a player may have had more streaks of bad luck than usual. We can expect him to have a better hitting percentage next year as his bad luck won't last forever.

For example, of the 10 major leaguers with the best slugging percentage in 2014, 9 were hitting the best of their careers, which was above their ability. And, of course, the results of these nine players in 2015, as expected, dropped to the average.

Of course, all players have different abilities, so results depend on both the individual's natural ability and luck in the aggregate.

Exceptionally good or bad periods usually do not recur

All of this brings us to one of the main mistakes we make when we don't understand or take into account regression to the mean when evaluating results - why extremely good or bad results are not repeated.

Looking again at examples from sports, there are a lot of superstitions that confirm the impossibility of repeating exceptionally successful results. There is the “Curse of the Rookie of the Year”, according to which the results of a rookie in the second season are much weaker. There's the "Sports Illustrated Curse" whereby a player who makes the cover of the magazine typically won't be as successful in subsequent seasons.

Of course, in reality all these are not “curses” and there is nothing supernatural about it. These are simply all examples of regression to the mean.

Remember that the same is true for the “losers”, although there are not many titled athletes among them. However, an exceptionally poor performance is usually not repeated, and subsequent effort and work on the game will usually result in results that reflect the individual's true abilities.

What does regression to the mean actually mean?

Regression to the mean affects variations in results in different areas, for example:

- Higher education students who received the highest grades in the middle of the semester usually do not perform as well on final exams. Luck helped them once, but is unlikely to help them again.

- Companies with the best profit margins in one year tend not to maintain the same results in the next.

- New drugs that show the most promise in clinical trials tend to show less impressive results when they go on the market.

- Tall parents tend to have children taller than average height, but not necessarily taller than their parents. The same goes for short people.

- Promising applicants, as a rule, turn out to be far from their super high expectations.

- Abnormally high or low blood test results may lead to a false diagnosis if they are random deviations from the patient's true mean.

Regression to the mean does not mean that everyone will always perform the same uniformly. Anyone's outstanding performance this year is unlikely to be repeated next year, but equally outstanding performance will be repeated by other people, teams, companies, and so on. Thus, the average to which all performances regress is the actual level of the individual or company, not the average of all people or companies in a particular industry.

Of course, abilities can change over time, but for ease of illustration in this article we have assumed that they remain constant.

conclusions

Because many of us mistakenly think that exceptional results accurately reflect people's abilities and will therefore be repeated, we are susceptible to all sorts of misconceptions about what prevents us from repeating past success.

For example, if struggling students are tutored and then perform better on exams, we tend to think that the intervention clearly had some effect, when in fact the truth lies in the usual outlier of variance, and the tutor may have conveyed nothing to the student at all. new.

If the best players or teams don't repeat their championship performances, we might think they've become complacent or arrogant or jinxed, when in fact they've just been as unlucky as they were last time.

This is where we will finish talking about theory and sports examples, and in the next article we will turn directly to poker.

Multa renascentur quae iam cecidere, cadentque

quae nunc sunt in honore vocabulae…

Many of the fallen will rise,

and many who are now on horseback will fall...

Horace, Ars Poetica

In 1886-1889, the English researcher Francis Galton carried out a series of measurements. He studied 205 pairs of parents and 930 of their adult children and published a series of articles in which he formulated the “law of regression to the mean” or, as it is sometimes translated: “the law of regression to mediocrity.” “For many continuous traits, such as height and intelligence, the adult offspring of a given parent have been found to deviate less from the population mean than the parent, that is, the offspring “regress” toward the population mean.

Two economists, Werner De Bondt and Richard Thaler, proposed in 1985 that investors overreact to random short-term fluctuations in stock prices, and this overreaction causes a company's market price to fall below its true value. Over time, the share price regresses back to its true value. Thus, stocks whose price has risen or fallen significantly will expect a large movement in the opposite direction. To test this idea, they took information from 1926 to 1982 and formed a portfolio of 35 companies whose shares rose the most in price and 35 companies whose shares fell the most. Once the portfolio was created, they analyzed its performance over the next 36 months. Research results showed that a portfolio of stocks that fell the most in price, 36 months after the creation of the portfolio, showed better results than those that increased in price the most (Figure 5.1). They explained this by saying that investors are too focused on short-term gains and are too optimistic in the short term.

In 1987 they returned to research again. Since investors can often overreact to events and sometimes be too optimistic when it comes to earnings, De Bondt and Thaler decided to copy the original stock portfolios but instead research the company's share price.

The research results showed that a portfolio of stocks that fell the most in price, in which the last three years of profit fell by 72%, and in the next four years showed an increase in profit of 234.5%. While the portfolio's return on winning stocks fell by 12.3% over the next four years (Figure 5.2). They explained this by saying that companies in a portfolio of losing stocks tend to have lower P/B growth rates than a portfolio of winning stocks. And therefore it is easier for them to show the best results in a short time.

To prove this, De Bondt and Thaler conducted a new study. This time, they categorized stocks by their price-to-book value, selected the five cheapest stocks and the five most expensive stocks, and created two portfolios. One is an undervalued company, and the second is an overvalued one.

In the graph (Figure 5.3) you can see that the portfolio of undervalued companies grew faster than that of overvalued ones.

Research by De Bondt and Thaler shows that stocks also follow the law of regression to the mean. A big rise or fall does not last long and after such movements, stocks tend to regress in the opposite direction, which is why they become the target of activist investors, since the business and security cycle is on their side. Original article

Stay up to date with all the important events of United Traders - subscribe to our